富裕層がターゲット 税務当局による情報・調査の包囲網

国際相続・国際資産税税務当局は、税務調査の重点調査項目として「富裕層」「国際」「無申告」への対応を掲げています。富裕層に対する税務調査が、年々強化されています。

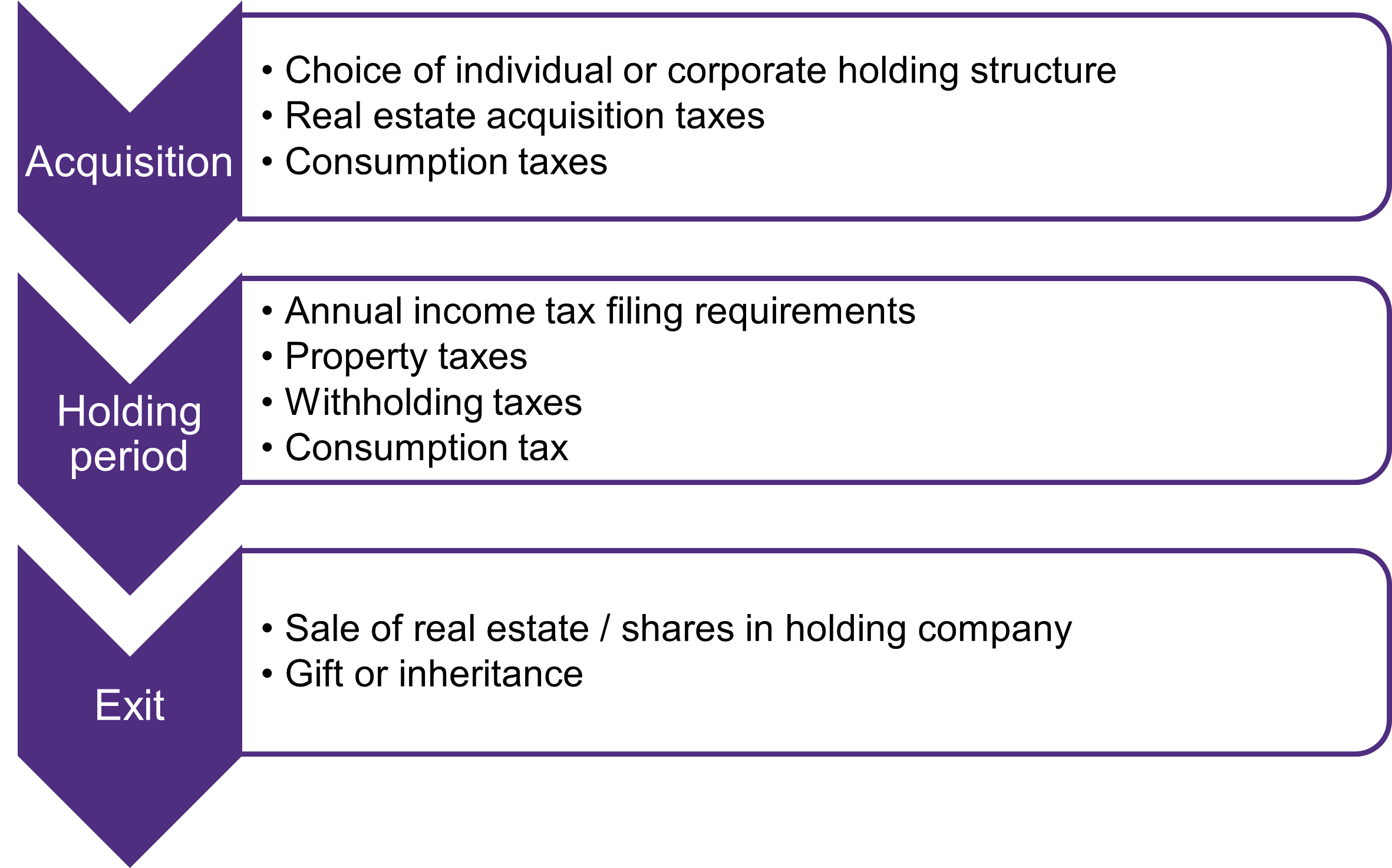

Foreign investors looking to invest in Japan real estate have various options on how to hold the investment. Generally speaking the taxation aspects over the lifetime of the investment are as follows:

The second in our series of newsletters covers the acquisition taxes and annual tax compliance associated with investing in real estate in Japan.

Real estate acquisition tax is due at 4% on residential land and housing (3% up to 31 March 2024) and 4% on other properties.

Consumption tax of 10% is due on the price of buildings but not land.

Registration taxes are due when the ownership of land and property is changed. The amount depends on whether the real estate is newly-built or used.

Stamp duty is paid by affixing stamps to the physical copies of the buyer and seller’s contracts. The amount depends on the contract value but ranges from JPY200 up to JPY480,000 for contracts over JPY5 billion.

Assets held as of 1 January each year are subject to fixed assets tax. The tax is 1.4% of the taxable base, which is calculated on the basis of a valuation made by the municipality and is usually lower than market value. Payments of the tax are due in four instalments in April, July and December of the year and February of the following year.

Our previous newsletter covered the different income tax rates for corporations and individuals. A non-resident individual is required to file an individual income tax return covering taxable income for a calendar year, and pay the income tax due by 15 March of the following year. A domestic corporation is required to file a corporate income tax return (including national, municipal and local returns) and pay the tax within 2 months of the end of the company’s financial year end. A one-month extension is available for the filing (but not payment) deadline.

Consumption tax of 10% should be charged on rental fees for commercial properties, but not residential ones. Consumption tax paid on purchases can be deducted from this. A consumption tax return and payment of tax is due at the same time as the income tax returns. In some cases, although the tax must be charged, a taxpayer may not be obliged to file a return and pay the tax over to the government. The obligation to file a return is complicated and depends on the type of taxpayer, taxable sales in previous periods and can also be affected by the type of tenants. It is advisable to take professional advice before purchasing a property in order to understand these various impacts.

Corporate tenants are required to withhold 20.42% of rental payments to a non-resident individual (10.21% for payments to non-resident corporations) as income tax. Individual tenants are not required to perform income tax withholding. No withholding is required if the landlord is a domestic corporation.

As you can see, there are many taxes involved in the acquisition and holding phase of property investment in Japan and professional advice should be taken to make sure these are understood at the planning stage. Stay tuned for the next newsletter in our series, which will cover the taxes upon exiting the investment.

税務当局は、税務調査の重点調査項目として「富裕層」「国際」「無申告」への対応を掲げています。富裕層に対する税務調査が、年々強化されています。

Foreign investors looking to invest in Japan real estate have various options on how to hold the investment.

If you are interested in receiving our latest insights, You can sign up to our mailing list.